|

Management of Intellectual Capital- Part I |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Knowledge

has become the most important fact of economic life of organizations.

Today the concern of organization along with earning profits and being

economically viable is to retain and exploit the talent of the people who

work in the organization; to gain the loyalty of the customers it serves

and learns from; to estimate and increase the value of its brands,

copyrights, patents and other intellectual capital; to harness the

collective knowledge embodied in its systems, to keep its management

techniques, and history unique to itself. The above-mentioned are vital

assets that are rarely managed and almost never managed skillfully; this

is more true in the Indian context.

Need for Management of Intellectual capital:

With the share of intangible assets increasing in the

total assets of the organization, the traditional system of accounting and

reporting the performance of the firm becomes irrelevant in the present

context. However, most of the firms follow a traditional system of

accounting in their organization where only the tangible assets seem to

play a more dominating role in the value creation process.

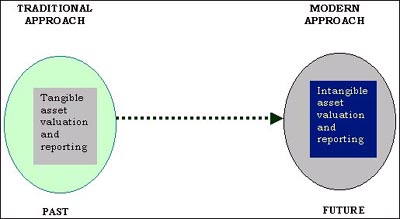

Change in Paradigm: Figure 1

However,

there is a constant need for creating awareness and see to it that there

is need that is generated at various levels of the organization to manage

intellectual capital in a strategic manner. This has been mainly the

result of the shift in paradigm from increasing role and importance of

intangibles in every organization. The change in paradigm is given in

Figure 1. It is necessary at this stage to briefly look at the evolution

of this concept as it is relatively new even in the western world. The

Table I gives a brief overview of the same.

Table

I: Evolution of Intellectual Capital Management

Having

discussed the evolution, now it's time to look into the basic

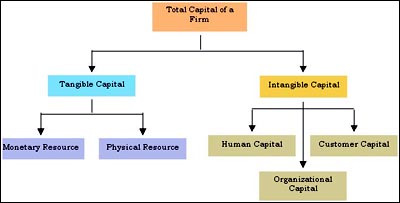

classification of the total assets of the organization. Mainly the value

for any firm whatever may be its basic function originates from its

processes. These may be considered as the total assets of the firm. A part

of the total is always in the form of tangible assets. These are the

physical infrastructure used in operations and the monetary investment

made to start and operate the functions of the organization.

More

important of the assets is that which most of the organizations ignore and

fail to manage. These are in the invisible form and intangible. These

extend from human capital to organizational capital to that of the

relational capital. They are varied and most difficult to assess and

measure though most of the organizations deal with them on a day to day

basis. The basic source of value for the firm is shown in Figure 2.

The relevance of the intellectual capital which is a

wider term than simple knowledge management has emerged from the ever

increasing competition faced by firms from the emerging globalization of

the world economies. The need to differentiate their firm and products

from that of the competitor, to increase the value of the firm, to retain

the existing base of the customers and to enhance the base further are

some of the drivers of the ICM.

Figure 2: Value of a Firm

Meaning

of Intellectual Capital:

Intellectual

capital was defined and classified in several ways by several researchers

since the concept gained importance. Edvinsson defined it as

"Knowledge that can be converted to value"[Edvinsson 1991].

Intellectual capital was the term, which was most used

in the early eighties and gained prominence in the late nineties. However,

Karl-Erik Sveiby first proposed a classification for Intellectual Capital

into three broad areas of intangibles namely Human capital, Structural

capital and Customer capital [Sveiby, 1989]; a classification that was

later modified and extended by replacing customer capital by relational

capital by Dr. Nick Bontis [Nick, 1991].

The International Federation of Accountants (IFAC) offers a slightly

different and broader classification as given below in Table II.

Human

capital

includes all the aspects related to the employees in the organization,

their training, development, their contribution to the organizational

development and also value creation, generation and sustenance. Thus, just

by having a large work force with good qualification and experience does

not amount to being efficient, Value creation Efficiency depends mainly

depends on the contribution of these employees towards value creation of

the organization(Edvinsson, 1997).

The Structural Capital refers to the organizational

structure, its vision, mission, infrastructure, Intellectual property that

the firm owns and the like.

Whereas, Customer or Relational capital is all

about the contribution of the clientele towards the organizational growth-

the amount of revenue generated through large customers, their commitment

levels measured thru repeat business, networking and the like is included

in this classification.

Though there are vast differences and varied opinion among

researchers and pioneers in the area of intellectual capital about the

items that should be included in each and the measurement tools that can

be used by the firms to report these, there is a general consensus on the

broad classification of Intellectual capital.

Having defined and classified the intellectual capital the

next logical question that arises is how is IC going to be measured? We

will answer this question in the next section.

References and Notes: |

Management of IC in your Organization:

The implementation of

the intellectual capital management requires building a model for its

functioning.

There are three different ways of moving ahead to develop a

model

1. Adjusting the conventional methods of accounting to

accommodate the new parameters and variables. Broadly considering the above aspects, the choice of method and model depends

on the following parameters [Steve 2001]. The IC Management Process:

The following aspects should be taken into account before

starting the process of management.

First, corporate strategy is guided by a vision of how a

firm, as a whole, will create value. Thus, both the tangible and intangible will

help in value creation and value realization. It is for the organization to

reinvent and realize the value of incorporating the intangibles in the

mainstream valuation and accounting.

Second, corporate strategy is a system of interdependent parts. Its success

depends not only on the quality of the individual elements but also on how the

elements reinforce one another.

Third, corporate strategy must be consistent with, and capitalize on,

opportunities outside the company.

Fourth, the benefits of corporate membership must be greater

than the costs.

Waiting for the right strategy discovery and then

implementation is not advisable, as there is no one way of arriving at the right

one. One has to get started first to develop any kind of strategy.

In the second step identify the variables that could be

measured.

Then decide on the methods that would be used to value them,

and then the estimation of the actual value is done.

Finally, it is accounted for in the company's annual

financial statement and therefore reported through formal channels to those who

decide the fate of the corporation: stakeholders, regulators and the society at

large.

Implementation of the model developed is more relevant than

the model itself. Therefore, usefulness of the model must be tested before

implementation. Moreover, the model depends on the nature of the industry and

its basic purpose. The IC model for the manufacturing unit is very different

from that of a service oriented industry.

This Table 1 illustrates a few basic differences in approach.

2. Retain traditional accounting and add new measures to account for

Intellectual Capital

3. Abandon old methods completely and have a new method

a. It should be auditable and reliable

b. It should not impose a large measurement overhead

c. It should facilitate strategic and tactical management

d. It should generate the required information to the shareholders

Table 1: Differences in Approach towards ICM

|

Service Oriented Industry |

Manufacture / Process Oriented Industry |

|

|

|

|

|

|

|

|

|

|

|

|

Despite the increasing

recognition of intangible assets within the corporate world, integrating them

with the strategic planning agenda inside a corporation often remains elusive.

Following are some of the common challenges faced by firms in Indian business

environment.

Lack of proper accounting and reporting may result in lack of

understanding by the investors and capital market to value the wealth of the

firm in its truest sense. This may either result in under valuation of the

firm's value or it's over valuation.

Inefficient or no valuation may cause significant damages to the

stakeholders and the company itself. Most companies do not have the knowledge of

what intellectual capital is; leave alone the aspect of managing it.

The solution lies in creating awareness on a large scale on

the opportunities that await for those who manage their intangibles. Awareness

should be concentrated in the areas of components that require measurement and

valuation and a standard format to report the intangibles value.

One ideal case in India is that of Infosys Technologies Ltd.,

which can be considered as an example for best practice in Intellectual Capital

Management (ICM).

Infosys is one of the pioneers in valuation and reporting of

intangibles in India. The annual report of the company incorporates these as an

invaluable asset of the company. The intangible assets of the company are

classified into four major categories – human resources, intellectual property

assets, internal assets and external assets.

Human resources

Human resources represent the collective expertise, innovation, leadership,

entrepreneurship and managerial skills endowed in the employees of an

organization.

Intellectual property assets

Intellectual property assets include know-how, copyrights,

patents, products and tools that are owned by a corporation. These assets are

valued based on their commercial potential. A corporation derives its revenues

from licensing these assets to outside users.

Internal assets

Internal assets are systems, technologies, methodologies,

processes and tools that are specific to an organization. These assets give the

organization a unique advantage over its competitors in the market place. These

assets are not licensed to outsiders. Examples of internal assets include

methodologies for assessing risk, methodologies for managing projects, risk

policies, and communication systems.

External assets

External assets are the market-related intangibles that enhance

the fitness of an organization for succeeding in the market place. Examples are

customer loyalty (reflected by the repeat business of the company) and brand

value.

Thus the company comprehensively encompasses all the aspects of intangibles.

The Intangible asset score sheet which is used at Infosys is

given below in Table 2

Table 2: Intangible Asset Score Sheet at Infosys Ltd. for the year 2002-03

|

Our

Clients |

2002-2003 |

Our

Organization |

2002-2003 |

Our

People |

2002-2003 |

|

Growth/Renewal |

|

IT

investment / value added (%) |

4.31 |

Education

Index of all staff |

44972 |

References:

1. Steve Pike, Anna Rylander, Goran Roos (2001),

"Intellectual Capital Management and Disclosure", in The Strategic

Management of Intellectual Capital and Organizational Knowledge: A selection of

Readings, (ed) Nick Bontis and Chun Wei Choo, Oxford University Press, New

York.

2. Infosys Technologies Ltd., Annual Report 2002-03

______________________________________________________________________________________________________________