|

Strategic Cost Management - A Bird's Eye View |

|||

|

|

|||

|

Strategic

cost management has become an essential area now days. While formulating

the strategy for the accomplishment of organizational overall objectives,

different cost driver should be clearly identified. Identification of key

cost drivers help companies to focus on key activities that will

constitute almost 90% of the total costs. In view of this, the importance

of strategic cost management should not be underestimated. This implies

that organization should be installing appropriate framework of strategic

cost management to reduce its costs in key areas on which the success of

organization is heavily dependent.

To give spotlight to the companies in this complex

business model we have covered some important aspects of strategic cost

management. Which can be very much help full to the business world. In

this paper we have tried to give some general explanation of strategic

cost management. We have first defined the meaning and applications of

strategic cost management and then we w3ent on to describe the framework

and steps involved in strategic cost management programme. And lastly we

have tried to identify some key enablers that will facilitate effective

implementation of strategic cost management programme along with the

questions that are to be answered while implementing strategic cost

management programme in an organization successfully.

Introduction:

Many of the terms are not new: cost reduction, target

costing, total cost management, or cost avoidance. These efforts have been

targeted in several organizations. But how many purchasing and supply

organizations have adopted these tactics for the short-term gain and how

many have taken a strategic approach that spans several links in the

supply chain? More and more will be taking the strategic approach,

focusing on strategic cost management. It has now a days become abuzz word

in the street of corporate houses. Corporate houses are now searching out

for ways to manage their huge conglomerates.

The downsizing and reengineering initiatives so prevalent

in the early '90s have largely proved financially short-sighted. With

hindsight, we now know that almost half of downsizing companies reported

lower profits the year following their cutbacks. Cost-cutters' stock

prices grew more slowly than those of companies which successfully grew

both their top and bottom lines. Less than one in five cost-cutters were

subsequently able to put their companies back on a profitable growth

track. Pressures on costs come from many external quarters, including

shifting customer priorities, the emergence of new competitors and

channels, and increasingly inquisitive financial mark.

Concept of Strategic Cost Management:

Trying to define strategic cost management requires

looking at today's leading organizations who are venturing in this area.

Some of the processes are new and uncharted territory, so there's no

textbook to spell it out.

Cost Management Defined:

The Purchasing Handbook defines cost management as, "the

establishment of programs that regularly analyze purchase requirements and

suppliers to identify lowest total cost and maximize total value to the

company. The development of a savings forecast by commodity is necessary

to define budget parameters for building cost-of-goods structures."

Strategic Cost Management:

Strategic cost management can be defined as"

scrutinizing every process within your organization, knocking down

departmental barriers, understanding your suppliers' business, and helping

improve their processes"

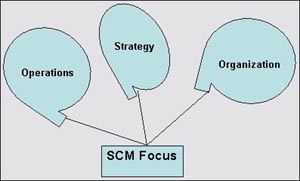

Applications of Strategic Cost Management:

There are three basic business areas where strategic cost

management can be applied.

Strategy:

A strategy in general terms refers to a plan of action

that will shape the direction of organization's success. Companies of late

have realized the importance of clear articulation of strategy and its

effective implementation. Before formulating any strategy, the management

should think about the business model whether it is still relevant or need

to be changed? Or whether the objectives of the business are going to be

accomplished through laid out strategy.

Operations: By

setting the priorities according to its significance we can operate the

tasks effectively and efficiently.

Organization:

Company should time and again check whether it is

allocating its limited resources in the businesses which generate more

value for the entire organization. Resources as such are the liming

factors for any organization and that's why the company should be

focus on the structure of the business and it should decide well in

advance whether it should own all resources or not?

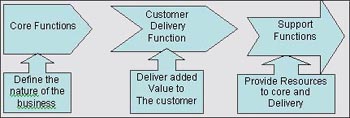

Strategic Cost management framework:

The Strategic cost management framework provides a clear

plan of attack for addressing costs and decisions that affect them.

Following are the three core components of this framework.

Core Functions: Core

functions elaborate on the nature of the business. It answers the very

obvious question what type of business are we in? At this stage the

company has to clearly identify its courses of actions with respect to

strategy planning, research and development, and product development.

Customer Delivery Function:

This step emphasizes more on value addition with various

activities such as marketing, sales, manufacturing, quality assurance and

control, sourcing, procurement and logistics, engineering and maintenance,

customer service and technical support etc. Excellence in those activities

can create a sort of competitive advantage for the company if it could

harness its resources intelligently than its competitors.

Support Functions:

As the name suggests, to support the core activities of

business some secondary activities are to be carried out which includes

IT, Finance and Accounting, HR management General administration. These

activities will facilitate the performance of the core activities in a way

that goals of the business can be accomplished successfully without

wasting limited resources. They will also help in synchronizing the

different tasks which are to be carried out simultaneously.

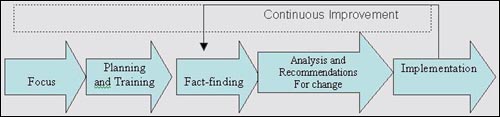

Strategic Management Programme Steps:

SCM Programme includes following five steps. These steps

can be detailed out as follows:

1. Focus: Focus

state starts with reviewing the different strategies of the company.

Reviewing the strategies will lead to clear identification of performance

gaps and this will help to bridge the gap by improving targets already set

beforehand. Modifying the targets will lead to developed plan of attack

which will foster better internal communication within the organization.

2. Planning and Training:

Planning plays a crucial role in implementing

strategic cost management programme. To implement the planning, a manager

should gather very efficient team members and train them accordingly.

Setting up of project management structure will facilitate the

implementation of strategic cost management by clearly identifying the day

to day activities, steering guidance and offering ad hoc assistance.

3. Fact Finding:

This stage includes the tasks such as data

gathering, conducting interview, developing benchmarks, conducting and

customer surveys.

4. Analysis and Recommendations for changes:

Analysis of activities plays a crucial role in

ascertaining the cost of the company. It can be done by various

strategic cost management analytical tools viz. cost driver analysis,

activity-based costing, selective business process reengineering etc. An

action plan for proposed change should address the following questions

what, who, when how aspects of the activities.

5. Implementation:

In implementation stage the first task to be done is

to define responsibilities and accountability of each individual and

controlling i.e. monitoring and corrective action should be the taken at

each stage of programme. And this is how the continuous improvement can be

achieved. The third, fourth and fifth sate in the above process indicates

continuous improvement.

Key Enablers That Facilitate Strategic Cost

Management.

Each individual organization needs to review their various

supply needs and supply chains and determine what enablers are of prime

importance to their situations. We will discuss an approach to that

problem later in the paper. In this section we will discuss a number of

generally applicable enablers, some of which are likely to be present in

many supply situations. The enablers are grouped by the three phases

present in most cost management approaches: analysis and planning,

implementation, and ongoing management and control. Some apply to more

than one phase and are so listed but discussed only at the first listing.

Analysis and Planning Enablers:

Sharing of Risks and Rewards - Necessary to the successful

integration of activities in a supply chain to achieve strategic cost

management in the chain. Provides all chain members with incentives to

cooperate and participate in cost management initiatives

Implementation Enablers:

Ask yourself the following questions to determine if

you're on a course for strategic cost management:

Organization and Personnel

Cost Improvement

Flexibility

Endpoint:

In today's era organizations are trying their hard to

reduce their costs. Ascertaining cost and finding out the ways to reduce

it has become the main issue for the organizations stepping into the

uncertain environment of 21st century. By following certain

steps and framework of cost management, an organization can effectively

and efficiently implement some good strategies related to reduction of

costs and that in turn will decide the future competitive advantage of the

companies trying to maintain their market share and brand image in the

tough competitive markets.

References: |