|

Understanding Working Capital Management |

|

|

|

|

|

On

the other hand going through some of the assignments submitted by students

specialising in HR at the MBA level convinces me of their abject ignorance

of Finance. How can these students ever go in for successful Strategic HR

interventions in the corporate world remains a major worry for teachers

like us? That is what got us thinking and hence this paper is addressed to

these managers in waiting as well. To begin with let the HR Manager (in

practice or in waiting) appreciate that the dark and dismal science of

economics is certainly not dark neither is it dismal. It is fairly exact

and very exciting provided the tools are in the hands of the right

craftsman and the teacher knows his subject. We have always opined that

people who are ill schooled in this fine subject should have sufficient

self-respect and refrain from teaching it. The younger generation deserves

this. We shall therefore begin with understanding some Economics (which we

consider the jewel in the crown of social sciences) and move through

common sense into one aspect of Financial Management (which is a

specialisation we consider to be bedrock of all managerial sciences). In

both instances mathematics is a language that the craftsman must

understand and learn to use judiciously. From a teacher's viewpoint the

author's advice to HR Managers (in practice and in waiting) is to get

their theory right since once theory is perfected reality would be unable

to hold out. Case studies are an excellent tool for teaching a subject provided

the theory has been understood. If not, they degenerate into story telling

sessions where the mouth starts to function long before the brain is

engaged into gear. This paper merely attempts to simplify the theory

behind working capital management for HR Managers in particular and

non-Finance Managers in general. Some basic premises of the Economic science also need to

be cited So you cannot say "I am investing two years of my time and Rs 2

Lakhs as fees in getting an MBA Degree." What you are doing is making

a financial outlay in the hope that the piece of paper (Diploma /Degree)

that you get at the end of the two-year period can be traded for a job in

the labour market. What you get by way of knowledge is abstract commodity

and it can well be argued that both the teacher and the taught are

partners in the expansion of knowledge. Machinery, goods in process,

inventory and buildings on the other hand are capital. Money is not

capital. In fact Crowther's famous poem is very helpful to recall at this

stage. So

the question rises as to what is working capital? Imagine a

four-legged table with a glass top. This is the euphemistic structure of

working capital. The first leg symbolizes cash and bank balances,

the second leg symbolizes Inventories, the third leg symbolizes

Receivables and the fourth leg symbolizes Investments. The

glass top symbolizes the allocation and utilization of scarce

available resources so that corporate objectives are met. The tabletop

made of brittle glass has to support some very heavy iron weights and to

top it all there is a glass of whisky on it. The glass of whisky is stable

so long as the four legs are equal and the top is even in surface. If any

leg were to be longer than the rest or shorter than them the whisky would

spill. If the table were weak and cannot support the weights then also the

whole structure would collapse. Now replace the wife with the shareholders and the iron

weights with your short-term liabilities. The dish of chicken with

additional business you never expected but now has to be financed and

which the four legs which stand for your assets would have to support. The

glass of whisky is replaced with profits. Now very simply, putting the

right weight, having a balanced table and enjoying your whisky and chicken

in peace is what working capital management amounts to. Keeping the

wife pleased is a bonus.

In short, it boils down to the management of funds in the short term as

opposed to managing long-term capital such as shares and debentures.

The HR Manager must appreciate that short-term capital has

to be repaid within a short period such as a year so its management is

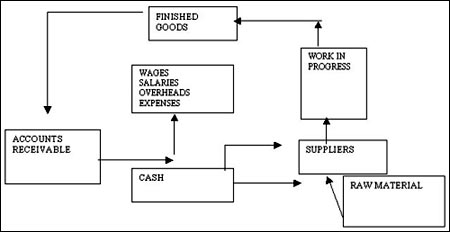

volatile. Working capital is after all the sum total of current assets,

which are used to pay back current liabilities and generate profits. The

goal of proper working management is to see that the current assets and

current liabilities are maintained in such a way that a satisfactory level

of working capital is maintained. It relates to funds in the short term or

a period normally one year and it is always transformed from cash into

other assets and back into cash within a business cycle.

Now let us see what the cash we need has to do with the

normal operating time often called the process cycle time. Some types of

businesses may have a longer operating cycle and this could be well more

than a year or even a decade as in the case of distilleries. Other

businesses may have a short operating cycle as a fast food store.

Working

capital could be either in terms of gross or net value. Whereas Gross

working capital is the total of current assets, Net working capital is the

total of current assets minus current liabilities. As a rule of thumb the

best possible practice is to see that there is sufficient liquidity to pay

back current liabilities without blocking too much funds. The trade off

between profitability and risk is the key to working capital management.

Anyone working with a fixed training budget would find this easy to

understand. Too little working capital increases profit but reduces

liquidity, as current assets are more expensive than fixed assets. For

instance if a management feels that worker training is a cost they will

apportion less funds for it. If on the other hand a management sees it as

an investment in manpower, the funds allocated would increase

substantially.

If

at a point of time the organisation does not have sufficient funds to meet

its short-term debts such as creditors and salaries as well as day-to-day

expenses it may become technically insolvent. On the other hand, if

it is very conservative it will have a surplus of working capital, which

will adversely affect profits. So it is easy to appreciate that the ratio

of fixed assets to current assets is a good measure of the balance to be

maintained.

There is no specific thumb rule. It varies from

industry to industry and the nature of business. Some industry norms are

given below. INDUSTRY

PROPORTION The ideal mix thus depends on the nature of the industry. Now we shall

very briefly take each component of working capital and see what are the

best practises adopted by industry in managing them.

Inventory is one of the most important components

of working capital and its proper management cannot be under stressed.

Fundamentally, inventory consists of raw material, work in progress and

finished goods. The proportion of inventories to fixed assets is quite

high ranging from 25% to 45% in the manufacturing sector (in cement it is

around 25%). Hence inventory management is crucial for all managers

irrespective of functional specialization. Since a number of industrial

relations disputes in manufacturing industries are linked to production

bonus and incentives relating to inventory irrespective of the market need

for inventory, the HR Manager must understand this point well. Every

member of the organization feels its impact and yet scant respect is paid

to it. This is most unfortunate. A serious study of sick companies will

support this contention. Hence those managers who are involved with

Strategic HR should take note of some of these important criteria for

insuring proper management. Further research by industrial economists sheds light on some practises

adopted by various industries, which are shown through extracts from their

balance sheets. Let us quickly glance at some of these important

indicators.

Accounts receivable : This also forms an

important part of working capital and depends on the credit policy adopted

by the firm namely Cash management: This as mentioned is the most

liquid of all assets and is required to Too much cash is not good nor is having too little a healthy practice.

Good companies usually have a practise to plant surplus cash in risk free

securities or inter company deposits. On the other hand, companies with a

deficit tend to borrow at a high rate of interest indicating a lack of

planning. A sudden surge in business may spur the need of working capital

and this may also require additional interest to be paid and again

planning is important.

The key to all management and especially working capital management is

to plan your work and then work to your plan. This also is an important

aspect of working capital management and good companies have the practise

of planning their needs well in advance.

Here is piece of advice to all those colleagues within

the HR fraternity. The next time your wife makes chicken and you invite

your colleagues over to your house for dinner and drinks, please remember

that this is all about working capital management. If they have a fun time

you are a damned good manager. If someone drops the glass or breaks your

table or slips and breaks his head then you know what to think of

your self. |